In a previous post here, I showed an assignat from 1792 and told the story of how the French revolutionary government used these papers to sell shares of confiscated property to the public. Only, they sold far more assignats than there was actual property, which led to that the assignats after a few years were practically worthless, ruining many of those who had bought them.

That was not the first time the French government pulled off a financial scam against its own population. Three quarters of a century earlier, 1716-1720, another episode took place, which likewise involved paper money and likewise ended in ruin for many.

First, let me show the banknote and describe its features. Then, if you are interested, you can read the background story below, involving the Scotsman John Law, the Mississippi company and the Mississippi bubble.

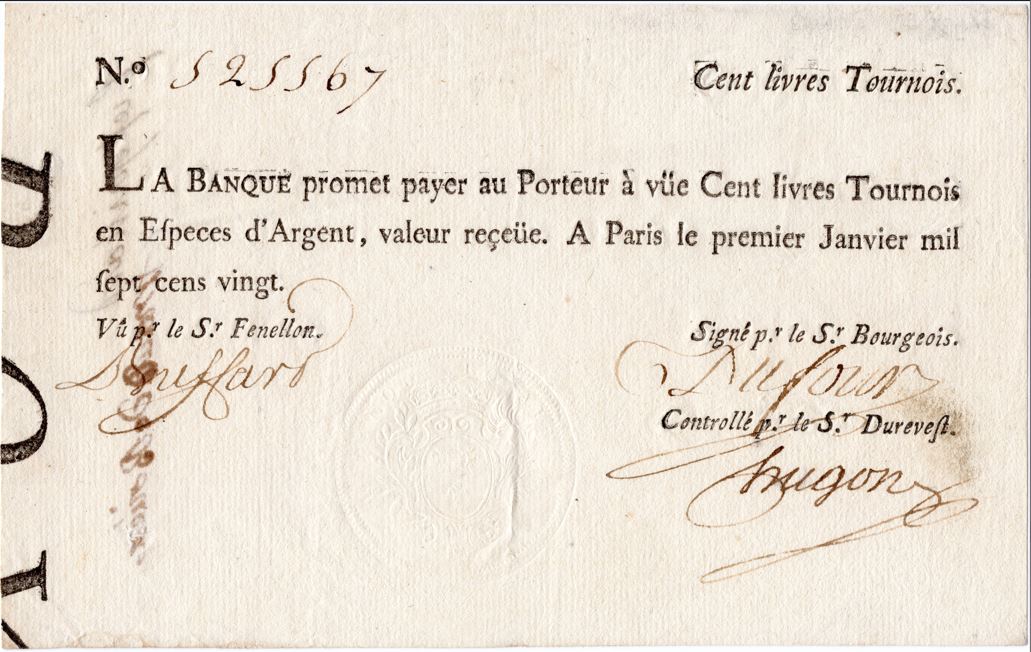

France 1720, 100 livres.

Not exactly the most stunning banknote we have seen here.

Very straightforward, just tells in small text (top right corner) that the value is

Hundred livres Tournois, then the bank's commitment:

THE BANK promises to pay to the Bearer at sight Hundred livres Tournois in silver specie, amount received, in Paris the first of January seventeen hundred twenty. Handwritten signatures by three clerks of the bank (named

Buffard,

Dufour, and

Hugon), on behalf of three more senior bank officials: Sires

Fenellon,

Bourgeois, and

Durevest. That those three officials needed to delegate the task of signing - to many more than the three named here - is easy to understand when we look at the (likewise handwritten) serial number of the note: 525,567. In all, there were 2,492,000 of these banknotes, all manually signed and numbered!

A few words about security features: The paper is watermarked (with the simple text

Billet de Banque) and has an embossing ("dry stamp", it can be seen between the signatures) showing the crowned royal arms and the text

BANQUE ROYALE. The black markings to the left are part of letters forming the text

BANQUEROYALE. The notes were cut (again, manually) from sheets, the cut going through the text and leaving a strip of paper where the corresponding serial numbers were to be found. That way, a banknote could be verified for authenticity by matching it with the cut.

The size is 16x10 cm (6.3x4 inches).

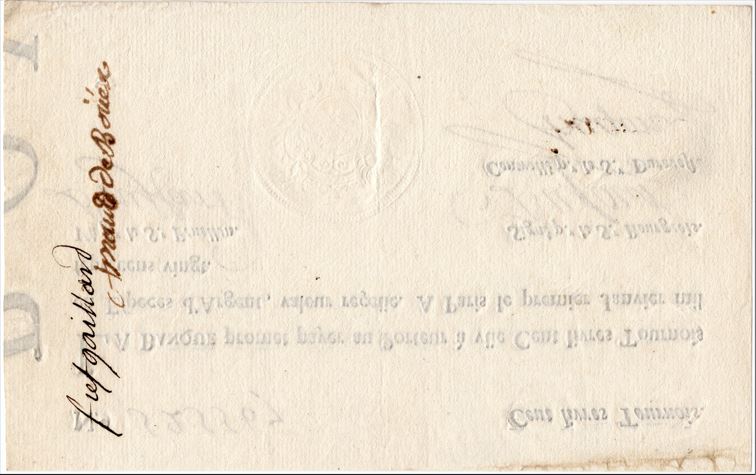

Here is the reverse:

The reverse is blank, but on this example there are two endorsements (cannot decipher them completely, but ending with

Gaillard and

de Bouee). Earlier papers, which were personal, required an endorsement to effect a transfer to another person. These banknotes, however, were payable to the bearer, so endorsement was not required. Regardless, it was not uncommon to do so as a simple protective measure. The signatures on the back showed the chain of owners and provided traceability, should the holder's ownership be questioned. To what extent this protective measure actually worked I do not know, but it was common enough that a decree was issued specifying that endorsements only indicated ownership and did not mean that the signer guaranteed the note's value.

In the case of this banknote, the second signature (de Bouee) could belong to the last owner, the person left with the note when it became more or less worthless (see background story below). Had it been brought to the bank for exchange, it would have been canceled by cutting off a corner.

Despite it being a not so uncommon procedure, few of these banknotes available on the market have endorsements.

Background storyIn 1715, king Louis XIV died. He left a France with miserable finances, ruined by decades of warfare, debts amounting to ten times the annual income of the state. His successor on the throne, his great-grandson Louis XV, was 5 years old, and naturally had little insights in state finances. The regent appointed to rule the country in his place, the Duke of Orleans Philippe II, was a prominent military leader and well versed in the arts, but running a country was a different challenge and bringing it out of financial chaos was certainly beyond his ability. Things didn't improve by his tendency to appoint ministers based on personal friendship rather than competence. State bankruptcy was considered a serious option.

Enter the Scotsman

John Law. Adventurer and mathematical genius, he fled England in 1695 to escape a death sentence after having killed a rival in a duel over a lady's favor. For twenty years he traveled across Europe, spending much time in Amsterdam and Paris. Using his talent for understanding probabilities, he amassed a fortune from gambling and speculation. More importantly, he formulated a theory for financial systems on a national level, with centralization, paper money, and liberal credits as central elements. He published treatises on this and searched for opportunities to try out his system in various countries. His ideas were ahead of his time, and he was turned down everywhere. Until 1716, in Paris. There the time and circumstances were right.

Law had made a name for himself in Paris already. His successful high-stake gambling, exquisite manners and winning ways caught the attention of Paris nobility and of the regent himself. Law now proposed his system to the regent, in the form of a central bank that would buy the state's debt papers in exchange for shares in the bank. A liberal credit system would stimulate the economy and its future profits would form part of the security for the banknotes. A bit shaky as that may seem to someone accustomed to regarding gold and silver as the only reliable guarantee of real value, it was a handy way out of the financial problems for the government and a state bankruptcy could be avoided.

The

Banque Generale was set up in May 1716. Shares in the bank could be bought by 1/4 specie and 3/4 government bonds, which provided an opportunity for investors to rid themselves of the potentially worthless bonds in exchange for potential profits from the bank's business. That was a smart move that quickly gave the bank a solid capital in specie. Its banknotes quickly became popular, since they were always redeemable in specie and provided a way to easily transport large sums of money across the country. The bank also provided credit and soon banknotes to a value ten times the bank's capital had been emitted, without the trust for the bank being reduced. The system seemed to work and everyone was happy.

In 1717 Law set up the West India Company (

Compagnie des Indes Occidentales), also known as the

Mississippi Company. Its purpose was to exploit the perceived riches of Louisiana and the Mississippi river basin, at that time French colonies. In 1718 the bank was transformed to

Banque Royale, becoming a state controlled bank, with part of its securities consisting of shares in the Mississippi Company. During 1719, the shares became subject to increased speculation, rising to 10, 20 and 35 times their nominal value. More and more company shares were emitted to meet the demand. The demand for banknotes increased too, and with the increased value of the bank's security in the form of inflated Mississippi Company shares, that demand could be met too.

Early 1720 things started to get out of hand. The Mississippi riches didn't seem to materialize, and the price of the shares began to fall. Law had by now advanced from bank manager to General Finance Controller of France, a position he used to enforce a number of measures to maintain his "system": To begin with, he fusioned the bank and the Mississippi Company. That had the effect that the declining confidence in the company spilled over to the bank, and its banknotes. It did not help that in order to stop the fall of the share price, Law enforced a fixed price of 9,000 livres for the shares. That only had the effect that the banknotes were dragged along in the fall and were accepted only with an increasing discount. To protect the banknotes and force their use, Law mandated that any payments above 100 livres be made with banknotes. Also, possession of more than 500 livres in coins was criminalized.

The falling value of shares and banknotes eroded the value of the bank's securities and in May 1720 a decree was issued stating that the banknotes were to have their nominal value stepwise decreased to only half by the end of the year. That triggered the burst of the bubble. Shares, and banknotes with them, fell to fractions of their earlier values, ruining many. That those who had speculated in company shares - and maybe had been millionaires on paper - lost their money, that could be tolerated. But that ordinary people, who did not take part in the speculation, but by law were forced to change their silver and gold into banknotes, also lost their savings, that was not seen kindly. In July, Law had to flee France to avoid being lynched, leaving his considerable fortune and properties behind. He died in 1729, without significant assets.